|

January 01, 2024

By

David

Messler -

Oil Price. Com

We’re on the Verge

of a Reset of Expectations in the Oil Sector

-

Oilfield services operators

focused on land-drilling could see the weakness they experienced in

Q-4, 2023, continue into Q-1, 2024.

-

Lower prices bring about a

sharp curtailment of drilling and a moderate reduction in completion

activity in shale.

-

Oilfield services sources:

we are just about in balance with legacy shale declines, drilling just

enough to move production higher incrementally higher.

Despite a late Santa rally in

the oilpatch this week, it's probably time to recognize that we are on

the verge of a reset of expectations for the oil sector in the

developing, likely 2024 price environment for WTI and Brent. We are

about one inventory build away from a trip back into the $60's for WTI

and the low $70's for Brent. Do we stay there for long? I doubt it,

and will discuss why in this article, but it could happen. In this

article I will discuss what I see as the most likely scenario for

2024.

The effect of lower prices on activity

The most probable scenario in my book is that lower prices bring about

a sharp curtailment of drilling and a moderate reduction in completion

activity in shale. Most of the shale drillers have a strong inventory

of drilling locations where capex is funded with WTI at $40. But

that’s a rainy day…or “rainy year” scenario, and doesn't mean the

CEO's of these companies won’t pull back funds if the current weakness

is sustained. In my view, if there’s any significant time in the $60's

for WTI, capex budgets are going to start being trimmed. Sub-sixty,

they will be slashed. Investors who have gotten used to hefty

dividends and massive debt and share count reductions over the past

couple of years will demand it. The old saying the "Cure for low

prices, is Low prices," is still true.

I discussed some of the challenges facing the U.S. shale industry in

an OilPrice article at mid-year. Thus far improvements in technology

and efficiency have kept this from occurring, but investors should

regard this roll-over as being delayed rather than cancelled. Industry

sources tell me that we are just about in balance with legacy shale

declines, drilling just enough to move production higher incrementally

higher. We've seen that over the past few months, with only the

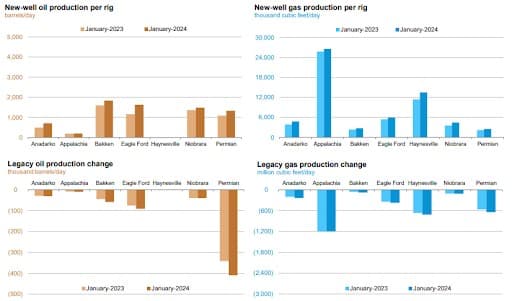

Permian and the Bakken adding net barrels incrementally.

For example, the chart above from the most

recent edition of the EIA-DPR, shows a net addition in the Permian of

760K BOEPD in 2023. That’s good, right? Deeper inspection shows that

much of this occurred in the first quarter of the year when the rig

count was 20% higher than today. Since July the count has been a 100

rigs below that figure, and since August it’s averaged around 150

below the 779 with which we started the year. To tie a bow on this

notion we can cite the Permian increase for December, 2023 at a measly

5K BOPD. This gives me confidence in my sources.

Related: Oil Prices Set for First Annual Decline Since 2020

Thank

heavens for the past couple of years though. Balance sheets are

repaired, debt maturity ladders are benevolent, and companies have

cash on the books, mostly. More importantly they have reconfigured

themselves to survive in a sub-$60's oil price scenario. They will

survive to see another day should that occur.

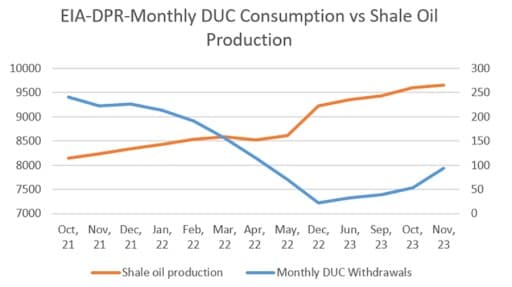

The first place capex will be cut is in drilling. Earlier this year

some folks were forecasting a ~50 rig pickup in 2024 to somewhere in

the 680 range. I think that's off the table over the short haul, that

we could be headed for a sub-600 rig count scenario. That will also

have an impact on the frackers, but not as extreme, at least in the

near term as there are DUCs to bring on. That won't have the runway it

did in 2020/22, as the DUC count is still way down, the industry only

added for a few months, before returning to withdrawals. From late

2020 to mid-2022 the DUC count fell from the mid-8,000's to the

mid-4,000's-pretty much where it stands as of now.

DUCs are not likely to be the complete panacea they were in 2021-2.

Remember we are starting at half the DUC inventory of 2021. There is

also a DUC "quality" issue with which to contend. The DUCs of today

are probably not as prolific as the one's Turned In-Line-TIL'd in

21-22. I have had conversations with production engineers that were

fairly disparaging toward the remaining DUC inventory. We may see!

In the graph above, note the rise in DUC withdrawal beginning in early

2023 as the rig count began to decline.

Your takeaway

I noted above that I felt drilling would take the major hit as

operators struggled to maintain output and cash flow in a sub-$60.00

oil price. Consistent with that belief I think the big land drillers,

Helmerich & Payne, (NYSE:HP), and Patterson UTI, (NYSE: PTEN) could

see the weakness they experienced in Q-4, 2023, continue into Q-1,

2024. The shares of both of these companies have declined by about 30%

over this period, and as I said may be subject to further weakness,

somewhat dependent on oil prices as we have discussed. My buy targets

for PTEN and HP are sub-$10 and sub-$30 respectively.

So I am cautious on the drillers presently, where am I looking for

short-term growth? One place is with the U.S. land frac’ers, with

Liberty Energy, (NYSE:LBRT) being a top pick at current levels.

Liberty is a segment leader and innovator with about a 20% market

share according to industry sources.

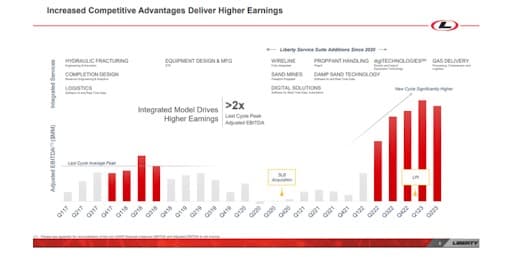

Liberty is crushing it with industry-leading Return on Capital

Employed, of 44% as reported in their Q-3, 2023 filing. Other earning

metrics are discussed in the slide below. One key statistic is the

rise in their EBITDA over time as they have integrated into being a

multi-service company.

The company has a number of

potential catalysts heading into 2024. One in particular that I will

highlight is Liberty has just inaugurated a new segment that I think

has the potential to drive revenues and margins higher in the New

Year.

I am referring to Liberty Power Innovations here. This is just an idea

whose time has come. With the focus on emissions related to frac'ing,

having mobile delivery of CNG-compressed natural gas, to the rig site

to run the pumps, is a stellar idea and one that should pay dividends

in the near future. A point worth making is that they are shifting

from a refined product that has been transported a number of times by

the time it reaches the rig, to a locally produced material that

requires relatively little treatment before being compressed. There is

efficiency in this alone.

Consider that a single frac fleet can consume 6-7 million gallons of

diesel annually, and you begin to have an idea of the amount of liquid

fuel that could be displaced by CNG. The linked article notes that 1

MCF of gas replaces about 8 gallons of diesel, a tremendous direct

savings with the gas selling for $2.5 MCF and diesel for $5.00 a

gallon. It's early days and I can't put a revenue or EBITDA on this

business. That said, it's a natural development given the macro

emissions reduction picture, and in my way of thinking comes with a

moat. I don't think this is readily replicable by other frackers.

Chris Wright, CEO comments on the course he sees for LPI:

“First to power our frac fleets. But it's also of course going to

supply other people's rigs, other operations in the field. There are

other oilfield applications for that. And ultimately as you look

ahead, what is Liberty generating expertise in. We're generating

expertise, and having the highest thermal efficiency on wheels, mobile

power generation there is. And we're generating expertise in how to

move natural gas, how to remotely or on-site process natural gas to

deliver natural gas, wherever it's needed and however it's needed.”

With the margins that Liberty delivers combined with innovations they

are rolling out, and a market biased toward their service segment, I

feel the shares of the company are significantly undervalued at

current levels.

Liberty is currently trading at an EV/EBITDA multiple of 2.5X on a Q-3

run rate basis. Analysts rate the company as Overweight with price

targets ranging from $20-27.00 per share. The company has a history of

beating analyst targets over the past year, and only seasonal weakness

might keep this from happening for Q-4. EPS forecasts are for $0.60

per share in Q-4, rising to $0.71 in Q-1, 2024. They easily beat

estimates in Q-4, 2022, and Q-1, 2023 so a trend is established. If

Liberty manages to beat in Q-4 then I think the company’s multiple

should rise. A 3X would easily deliver the lower range of the price

targets, and a 3.5X would put them in sight of the upper range.

None of these estimates take into account any revenue or margin growth

that the company has consistently exhibited over the past several

years. With that in mind, I have Liberty as a top pick. I think

investors with a modest risk tolerance should carefully consider if

the company meets their objectives.

By David Messler for Oilprice.com

Green Play Ammonia™, Yielder® NFuel Energy.

Spokane, Washington. 99212

509 995 1879

Cell, Pacific Time Zone.

General office:

509-254

6854

4501 East Trent

Ave.

Spokane, WA 99212

|