Shades Of Gray, Blue And Green: Future Of

(Sustainable) Hydrogen Economy BySarwant

Singh

June 01, 2023

There is a joke about hydrogen that has been doing the rounds for

close to three decades now. It goes something like this: Hydrogen is

only 10 years from commercialization. But then, it has always been

10 years away from commercialization. I believe this barb has outlived

its relevance.

Why am I convinced that hydrogen has finally arrived? Chalk it down to

a recent cross functional study on the Future

of Hydrogen Economy commissioned by,MarketsandMarkets which

revealed some surprising (and not so surprising) findings about the

opportunities and challenges linked to hydrogen commercialization.

Here are some key highlights from the study:

Market Size 2022 and 2035

MARKETS AND MARKETS

Upstream hydrogen generation reminds me of one of my favorite songs:

Mambo No. 5, albeit instead of a little bit of Angela, Pamela, Sandra

and Rita, you have a little bit of gray, blue and green hydrogen. Of

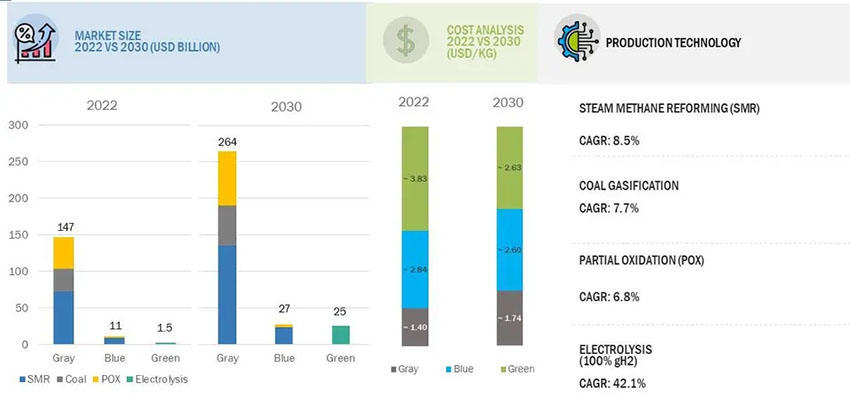

these, gray hydrogen is the most widely produced because of its cost

effectiveness and widespread availability. In 2022, around 92% of

hydrogen (by value) was gray hydrogen, underlining global dependence

on this carbon-intensive production process. By 2035, low to

zero-carbon emitting blue and green hydrogen are expected to pick up

pace and comprise about 22% of total hydrogen production.

The global hydrogen generation market is expected to grow from USD

159.5 billion in 2022 to USD 334 billion by 2030. Asia Pacific

currently dominates, led by countries like China and India that have

considerable capacity in ammonia production and refinery throughput. A

few blue hydrogen production technologies such as steam reforming, gas

heat reforming, and biomass gasification with technology readiness

levels (TRL) of less than 7 will play a crucial role in the hydrogen

economy by 2030. Rising environmental awareness, coupled with the EUs

binding target of effecting at least a 40% reduction in greenhouse gas

emissions by 2030, underpin Europes lead in blue and green hydrogen

generation. The Netherlands and Germany are the largest markets for

blue and green hydrogen in the region, respectively.

One of the main dilemmas is the multiplicity of technology choices for

hydrogen production: steam methane reforming (SMR), coal gasification,

partial oxidation, and electrolysis - the most expensive but also most

environmentally friendly production technology - for gray hydrogen

together with PEM, alkaline electrolyzers, solid oxide electrolyzers (SOE),

and anion membrane electrolyzers for green hydrogen (see chart below).

An array of choices worthy of Mambo No. 5!

In terms of green hydrogen production technologies, alkaline

electrolyzers will remain the largest market, swelling to USD 15

billion by 2030. China will look to this technology to boost

manufacturing capacity of green hydrogen from around 5.4 GW in 2022 to

an estimated 100,000200,000 tons by 2025. Alkaline electrolyzers will

grow marginally faster than competing technologies like PEM over

2022-2030, primarily due to $/kg factors. Post 2030, new technologies

will play a more prominent role.

SOE will be a major focus area in Europe backed by its high efficiency

of 8085% relative to other solutions. Nevertheless, as the chart

reveals, it will still constitute a comparatively smaller share of the

overall green hydrogen production technology market.

Midstream - Conversion,

Storage and Distribution Challenges

The cost of

producing hydrogen is equivalent to the landed cost of converting,

storing and transporting it. It costs roughly around $2.37/kg to

produce liquid hydrogen and about the same amount to convert, store,

transport, and then re-convert it.. Similarly, while it is slightly

cheaper to produce, convert, store and transport hydrogen produced

from ammonia than it is from liquid hydrogen, this is neutralized by

higher re-conversion costs. Hydrogen is, therefore, disadvantaged in

terms of cost competitiveness compared to other energy sources that

are significantly cheaper to store and transport.

Concerns linked to transportation also remain a critical consideration

in overall infrastructure development. The choices fall between

pipeline delivery and liquid tankers for long distance transportation.

Meanwhile, cost reduction in electrolysis technology will drive demand

for onsite hydrogen supply fueling stations.

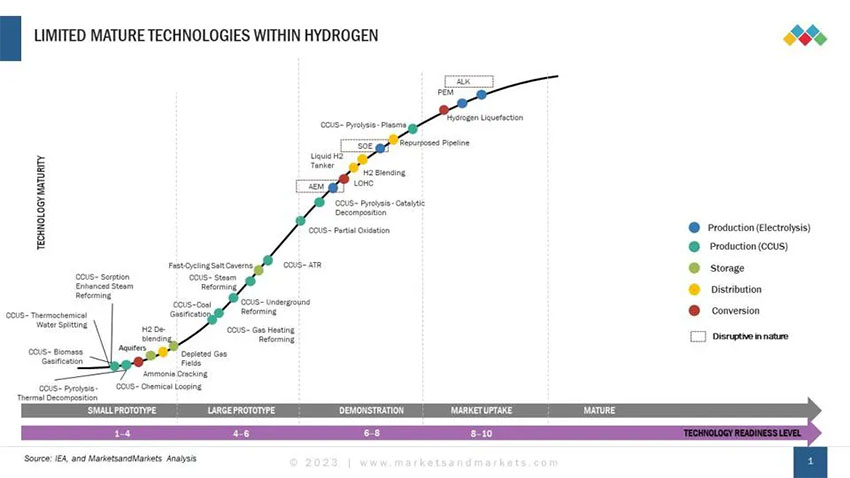

Hydrogen Technology Portfolio Life Cycle Analysis MARKETS

AND MARKETS

The lack of hydrogen refueling stations presents another stumbling

block. Targeted investments will be required to increase coverage and

boost confidence among end user sectors like automotive. Today, much

like my cricket batting average which hovers in the lower double

digits, most countries have fewer than 100 stations, many of which are

not even fully functional. Of the 15 hydrogen refueling stations in

the UK, for instance, a few have already shuttered. On the other end

of the scale, Japan which has made hydrogen a lynchpin in its clean

energy strategy, stands out with 165 stations. MarketsandMarkets

forecast about 18,000 fueling stations globally by the end of 2030, a

number which pales in comparison to the robust infrastructure

available for fossil fuels and electric vehicles (EVs).

In short, it would be hard to make a compelling business case for

shipping green hydrogen from, say, Australia to Europe. That said,

challenges related to conversion, storage, and distribution open up

opportunities for business model innovation. MarketsandMarkets

envisions a business model where hydrogen generation and consumption

occur at site. This is a potential game-changer since it unlocks a

realm of new possibilities where airports, ports and, potentially,

even the military could be both producers and consumers, creating a

springboard for a localized hydrogen economy.

Downstream The

Excitement Begins

A shift to green hydrogen offers the prospect of slashing total carbon

emissions estimated at over 50 gigatons globally in 2022 by nearly

1 GT in just chemical and industrial applications, before effecting

sizeable carbon reductions across power, transportation, and

construction and other industries by 2050.

The chemical industry stands to be one of the biggest beneficiaries of

a hydrogen economy, realizing end-to-end green labelling for key

chemicals like ammonium sulphate, ammonium nitrate, and methanol

derivatives. Ammonia production is set to generate demand for blue and

green hydrogen to the tune of nearly 13.2 million metric tons (MMT) by

2035. Simultaneously, the increasing penetration of e-methanol from

current levels of less than 1% to 20% by 2035 is projected to push

demand for green hydrogen to 8 MMT.

Green hydrogen is also poised to catalyze decarbonization initiatives

in the steel and semiconductor industries. Green steel which uses

hydrogen to achieve a minimized carbon footprint is currently under

development. Penetration rates are set to grow to 10%, driving annual

demand for green hydrogen to 15 MMT by 2050. Demand from the

semiconductor industry is also projected to spike due to hydrogens

role as both carrier and process gas in chip manufacture.

Another industry which will be significantly impacted by hydrogen is

the automotive industry. The number of hydrogen powered fuel cell

vehicles is expected to surge from 20,000 units in 2022 to around 1.28

million units by 2035. Such forecasts are based on the substantial

volume of long distance and heavy-duty fleets, including buses,

light-, medium- and heavy-duty trucks which require a sustainable

powertrain. While the Asia-Pacific region is focusing on passenger

vehicles, the US and EU will concentrate predominantly on commercial

vehicle applications.

I believe there is an abundance of exciting use cases for hydrogen in

energy, ports, aviation, marine, defense, space, and unmanned

vehicles, among others. A hydrogen-based hyper sonic plane that can

take you from Australia to the UK in two hours? Swiss aerospace

company Destinus aims

to do just that with its Mach 5 hypersonic passenger aircraft fuelled

by hydrogen for ultra-long-range transportation.

Even more fascinating is the innovation that will occur in hydrogen

specific vehicle platform and architecture strategies. Like EV

skateboards developed in passenger vehicles, hydrogen will herald in

new commercial vehicle platforms that integrate the fuel cell systems

into new product categories that will optimise the balance of range

vs. refuelling vs. payload.

China vs the Rest of

World (RoW): The Race Continues

Chinas aggressive & successful industrial policies related to solar,

wind, and battery technologies are well documented. Will it be a

reprise when it comes to hydrogen? The short answer: Yes. The longer

one is that they are already there. Europe, for example, is expected

to turn to China whose solutions focus primarily on hydrogen as a

sustainable energy carrier rather than a commodity.

Chinas strategy, as we saw with electric batteries, has been to bet

to one horse (technology), drive economies of scale, reduce costs, and

own the entire supply chain. A case in point is its monopoly over

lithium iron phosphate (LFP) batteries rather then the more expensive,

but energy efficient & technically better nickel manganese cobalt (NMC)

batteries. Similarly, in hydrogen, China is expected to bet on

Alkaline electrolysers and has the ability to develop alkaline

electrolysers at <30% of EU costs, although it is not yet competitive

in terms of PEM and SOE.

This past weekend, a liquid hydrogen-powered car made its debut at a

24-hour endurance race in Japan. From 2026, hydrogen-powered cars will

be allowed to participate at the gruelling Le Mans competition. Its a

race to the finish and to stay ahead, the West needs smarts, speed,

and stamina to develop energy efficient technologies like SOE at

competitive price, or run the risk of being second place finisher, yet

again in what will be an important source of energy in the future.